Get your 409a Report

A 409A valuation report determines the fair market value (FMV) of a private company’s common stock to comply with IRS Section 409A regulations. It ensures that stock options are priced accurately and helps companies avoid tax penalties. The report typically includes the valuation’s purpose and scope, company overview, capital structure, financial analysis, industry outlook, and applied valuation methodologies such as the market or income approach. It concludes with a final FMV per share, analyst’s certification, and compliance statement to provide IRS “safe harbor” protection and support accurate equity-based compensation decisions.

Different stages of a business when 409A analysis is required:

Startup/Early Stage: When the company first plans to issue stock options to employees or advisors to comply with tax regulations.

Post-Funding Rounds: After each financing round (seed, Series A, B, etc.) to reflect updated valuations and set option strike prices.

Pre-IPO: Before going public to establish the FMV for equity compensation in preparation for the IPO.

Acquisitions/Mergers: During or prior to a change in control or sale to assess valuation for stock-based consideration or new compensation plans.

Significant Business Changes: When there are material changes in financial performance, business model, or market conditions that impact valuation.

Annual/Periodic Updates: Many companies perform 409A valuations at least annually or more frequently if significant corporate events occur.

These stages ensure compliance with IRS rules, provide defensible valuations, and maintain proper accounting for stock-based compensation.

Who Needs 409A Reports?

Private companies planning to issue stock options or equity-based compensation must obtain a 409A valuation report. This report is mandatory under IRS Section 409A to determine the fair market value (FMV) of the company’s common stock. It applies to companies awarding equity to employees, founders, consultants, and directors. Startups and early-stage companies especially require a 409A valuation before issuing their first stock options.

The valuation must be updated at least once every 12 months or following any material event impacting company value, such as funding rounds, mergers, acquisitions, or major operational changes. An independent appraisal by a qualified third party provides safe harbor protection from IRS penalties and ensures compliance with tax regulations.

Without a 409A valuation, companies and recipients of stock options risk severe tax consequences, including immediate taxation and penalties. These valuations protect legal compliance, foster investor confidence, and establish fair, transparent equity compensation practices essential for startup growth and corporate governance.

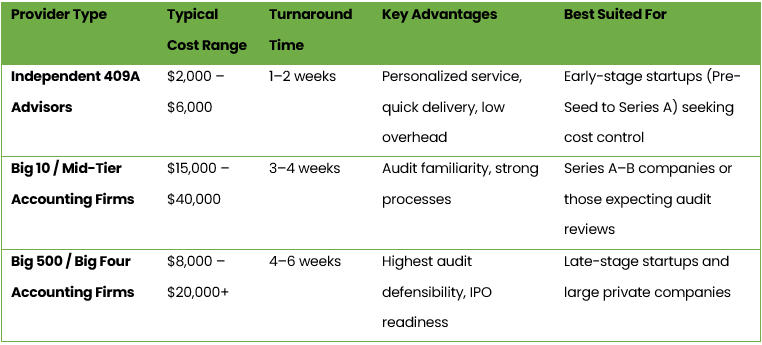

409A valuation pricing differs significantly among independent valuation advisors, Big 10/mid-tier firms, and the largest global accounting firms.

Key Observations

· Big Four firms are often 6–10 times more expensive than independent advisors due to more extensive documentation, multi-level reviews, and stronger brand credibility.

· Independent advisors typically offer the fastest turnaround and personalized attention, while Big firms take longer due to rigorous processes.

· Large accounting firms are recommended for companies expecting external audits, IPOs, or complex capital structures, whereas independents are usually sufficient for internal compliance and early-stage needs.

· Mid-tier firms offer a middle ground between cost and rigor, suitable for growing startups at pivotal funding stages.

409A Valuation Cost Comparison (2025)